Retirement Savings Accounts

Learn how and where to save to fund your retirement. Use 401(k)s, traditional and Roth IRAs, HSAs, and other tax-advantaged accounts strategically and set the financial goals you need to establish your future.

:max_bytes(150000):strip_icc()/thinkstockphotos-89518198-5bfc347646e0fb0083c21b58.jpg)

:max_bytes(150000):strip_icc()/GettyImages-1135289130-1344cc1e180a49ab9c87b20cf0dd9904.jpg)

:max_bytes(150000):strip_icc()/retirement-planning_86520349-5bfc2b3bc9e77c002630567c.jpg)

:max_bytes(150000):strip_icc()/thinkstockphotos187320972-5bfc3d2646e0fb0026604f00.jpg)

:max_bytes(150000):strip_icc()/GettyImages-1166987219-69a5b981ab0946a4a7a90a6b3395c11a.jpg)

-

How much of your salary should you save for retirement?

Research says you need to save roughly 15% of your annual salary—but if you wait until you’re older to save, you will need to save more. The goal: to have an income that’s 75% to 80% of what you brought in the year before you retired.

-

How do you retire if you have no savings?

You’ll need to scale back, downsize, and possibly continue working part-time. Taking a roommate may help—and a reverse mortgage is an option if you own your home.

Learn More: Retirement Without Savings? -

What’s the best way to start saving for retirement?

Just start—and take advantage of employer-based matching funds in your 401(k) if you have one. If not, consider a Roth IRA if you qualify, or a traditional IRA if you want the tax deduction. Brokerage firms have many options to explore.

Learn More: Starting a Retirement Fund: How To Start Saving -

How do I use my HSA when I’m retired?

You can contribute to your Health Savings Account until you start taking Medicare and take tax-free withdrawals to pay qualified medical expenses. This is better than 401(k) and traditional IRA distributions, which are taxable.

-

What’s the difference between a 457 plan and a 403(b) plan?

Public-sector and not-for-profit organizations cannot offer 401(k) plans. A 403(b) plan is typically offered to employees of private nonprofits and government workers, including public-school employees. There are two different types of 457 plans—the 457(b) to state and local government employees and the 457(f) to top executives at nonprofits.

Learn More: 457 Plan vs. 403(b) Plan -

What kind of retirement can you have on $1 million?

Even $1 million requires smart budgeting. Retirees will probably do better and have more flexibility if they invest in a traditional portfolio and take yearly withdrawals rather than buy an annuity.

Learn More: This Is How Retirees Live on $1 Million

-

Profit-Sharing Plan

This plan lets employees share in company profits based on quarterly or annual earnings. The company makes contributions to the plan; employees cannot.

-

Rule 72(t)

This allows account holders to take early penalty-free withdrawals from IRAs and other tax-advantaged retirement accounts according to specific rules.

-

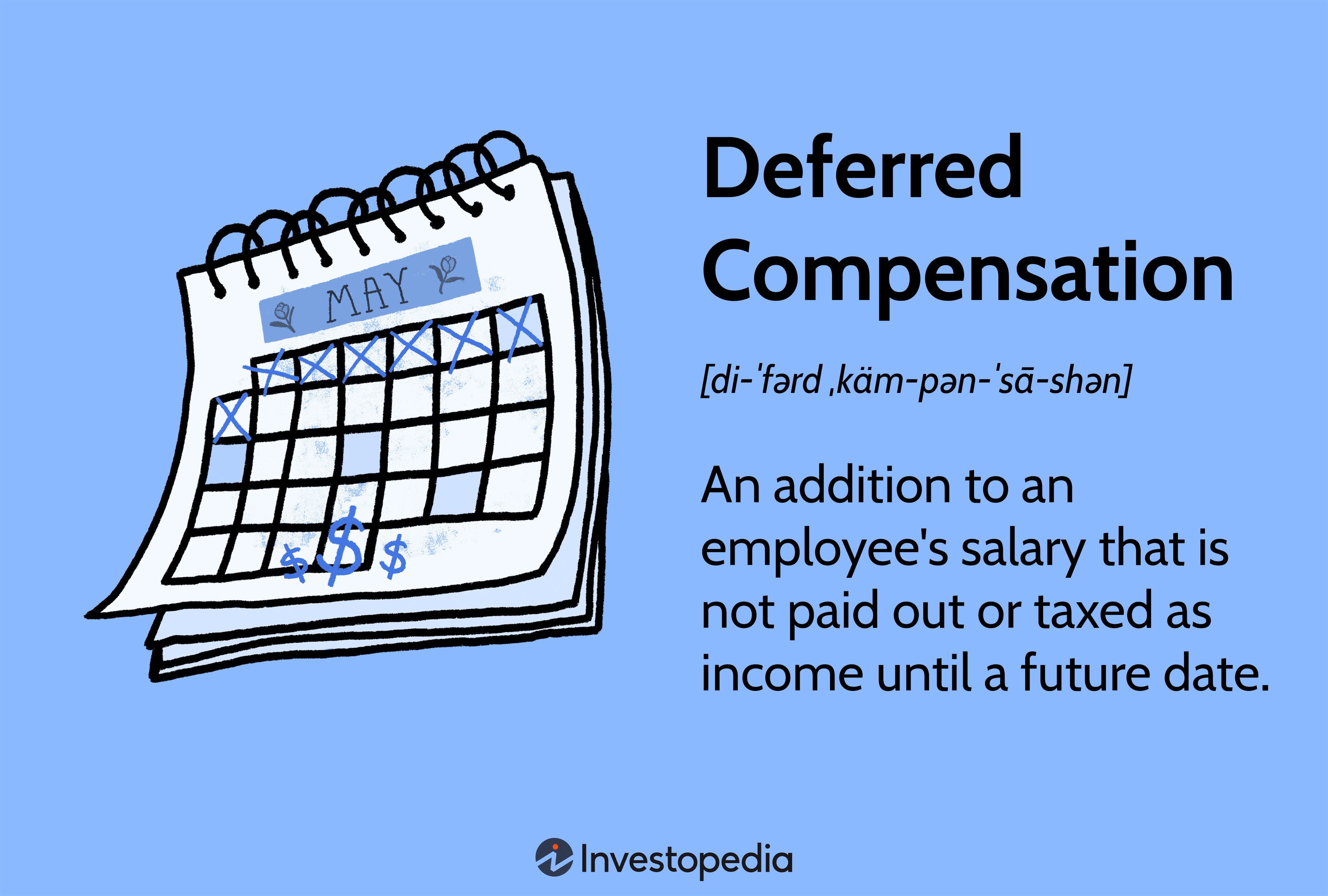

Deferred Compensation

These plans allow employees to defer compensation—and the taxes due on them—until they retire. There are qualified plans, such as 401(k)s and non-qualified plans, which some companies make available to highly compensated employees.

-

Non-Qualified Plan

These are tax-deferred, employer-sponsored retirement plans that fall outside of ERISA guidelines and are offered to key employees and others, often as a recruitment or retention tool. There are four types.

-

Qualified Retirement Plan

These retirement plans meet IRS requirements and include 401(k)s and 403(b)s. Both employers and employees get tax benefits for offering and contributing to these plans.

-

Cliff Vesting

This practice gives employees the right to receive full benefits from their company’s retirement plan at a specified date, often after five years, rather than becoming vested gradually over a period of time. It applies to both qualified retirement plans and pension plans.

-

Pretax Contribution

A pretax contribution is any contribution made to a designated pension plan, retirement account, or another tax-deferred investment vehicle for which the contribution is made before federal and municipal taxes are deducted.

:max_bytes(150000):strip_icc()/GettyImages-1207388625-b712a50a55554c2c876a0085ee15faab.jpg)

:max_bytes(150000):strip_icc()/5271919-GettyImages-1151630025-a67dda7082f94cadb756317861fc3b30.jpg)

:max_bytes(150000):strip_icc()/GettyImages-1292251389-0f571790df454c25bff892cf6509a0d4.jpg)

:max_bytes(150000):strip_icc()/Primary-Image-best-solo-401k-companies-5089155-dac51fb889314e1ab57e34b8ba759a9f.jpg)

:max_bytes(150000):strip_icc()/GettyImages-1310155824-0f0f43d84b284bedaab9fb425ca7cb72.jpg)

Explore Retirement Savings Accounts

:max_bytes(150000):strip_icc()/GettyImages-607477463-779ff25a1e8e40b2aa03648b678379fa.jpg)

:max_bytes(150000):strip_icc()/woman-s-hands-holds-small-green-plant-seedling-182253551-7ffe8395630945ca83a1335126782b23.jpg)

:max_bytes(150000):strip_icc()/78036503-5bfc2b8b4cedfd0026c118ed.jpg)

:max_bytes(150000):strip_icc()/GettyImages-1027141710-3fa5bf9c3b2843ea821fad9b84de396c.jpg)

:max_bytes(150000):strip_icc()/manager-is-holding-irc-section-72-t--documents--1017300642-353c6b131d844c29a9c5bc06a76a834d.jpg)

:max_bytes(150000):strip_icc()/thinkstockphotos-122413590-5bfc355246e0fb00265dc268.jpg)

:max_bytes(150000):strip_icc()/GettyImages-1131086835-83fd238d51f44798943a4e69c1198537.jpg)

:max_bytes(150000):strip_icc()/GettyImages-597316549-bbbf9f28dea9452fb0867f412c4f22f2.jpg)

:max_bytes(150000):strip_icc()/GettyImages-1133007677-22b35aad9da34a55989626cf40b8a456.jpg)

:max_bytes(150000):strip_icc()/hand-of-female-putting-coin-in-jar-with-money-stack-step-growing-growth-saving-money--concept-finance-business-investment-915075364-bd2a702aa38d4d2eb158178b6ecb5160.jpg)

:max_bytes(150000):strip_icc()/GettyImages-500924937-5aba51e4eb97de00362e7169.jpg)

:max_bytes(150000):strip_icc()/business-people-discussing-in-office-940682222-fc0cb4d7433d4d51921e11cc5271847c.jpg)

:max_bytes(150000):strip_icc()/200393273-001-5bfc2b8bc9e77c0026b4f8ce.jpg)

:max_bytes(150000):strip_icc()/403bplan_final-67070c84b22b42478c5bb4c12792995c.png)

:max_bytes(150000):strip_icc()/98054708-5bfc3881c9e77c0026b89124.jpg)

:max_bytes(150000):strip_icc()/profitsharingplan.asp-final-77a215fb826640de895198124604118c.png)

:max_bytes(150000):strip_icc()/retirement-lrg-2-5bfc2b1e46e0fb00260b1123.jpg)

:max_bytes(150000):strip_icc()/options-lrg-5bfc2b1f4cedfd0026c10437.jpg)

:max_bytes(150000):strip_icc()/istock_000057964752_medium-5bfc3c3c46e0fb00511dfa08.jpg)

:max_bytes(150000):strip_icc()/200275051-001-5bfc2b8b46e0fb0083c07b92.jpg)

:max_bytes(150000):strip_icc()/GettyImages-486435953-4059ec6817f64eda898c10f811b5bf02.jpg)

:max_bytes(150000):strip_icc()/shutterstock_143828704-5bfc3d2d46e0fb002605ea87.jpg)

:max_bytes(150000):strip_icc()/this_is_how_retirees_live_on_1million_dollars-5bfc3461c9e77c0051459152.jpg)

:max_bytes(150000):strip_icc()/GettyImages-1017300682-3086d9bb0cc942df8fc62401a5286372.jpg)

:max_bytes(150000):strip_icc()/retirment_plan_form-5bfc316e46e0fb00517d012c.jpg)

:max_bytes(150000):strip_icc()/GettyImages-932632502-04f920807f904eb4829ae79a655b78e8.jpg)

:max_bytes(150000):strip_icc()/thinkstockphotos78747101-5bfc3b4ac9e77c0051480b07.jpg)

:max_bytes(150000):strip_icc()/retirement_plan-5bfc329a46e0fb00511af7ef.jpg)

:max_bytes(150000):strip_icc()/GettyImages-982301414-403835b36b85415b81a528264fdbbb58.jpg)

:max_bytes(150000):strip_icc()/GettyImages-1287257611-2c76e99fa77a4cffa58a54ea2b197f86.jpg)

:max_bytes(150000):strip_icc()/retired-50s-medicare_122577774-5bfc2b3dc9e77c0026b4eb71.jpg)

:max_bytes(150000):strip_icc()/mutual_funds-5bfc2f87c9e77c0026b5b89d.jpg)

:max_bytes(150000):strip_icc()/charlesschwab_AP101007044882-539143ef33bf4f60ae2b6adcdfc2881f.jpg)

:max_bytes(150000):strip_icc()/istock-91516278.jygallery.retirement.funds.cropped-f371e09638144125b07585996450f7d7.jpg)

:max_bytes(150000):strip_icc()/their-finances-are-in-the-green-884678024-1dc8099a37264ca7bff10bfc170e6a99.jpg)

:max_bytes(150000):strip_icc()/rbv2_53-5bfc2b8ac9e77c0058770499.jpg)

:max_bytes(150000):strip_icc()/GettyImages-1072508860-73bcaf30d71c464e9bc969660979ec4c.jpg)

:max_bytes(150000):strip_icc()/mature-couple-canoeing-on-tranquil-lake--alberta--canada-1032682512-2468d5a1347a427e8c7cf3fc62c53968.jpg)

:max_bytes(150000):strip_icc()/141251781-5bfc2b9646e0fb00517be167.jpg)

:max_bytes(150000):strip_icc()/403_b_plans_-5bfc2f6346e0fb00511a625c.jpg)

:max_bytes(150000):strip_icc()/86807848_ComstockImages_Stockbyte_GettyImges-56a635823df78cf7728bd82d.jpg)

:max_bytes(150000):strip_icc()/GettyImages-1131086835-5998e1e5472f4d8c933f303554a9bc5f.jpg)

:max_bytes(150000):strip_icc()/shutterstock_2369793-5bfc3cdbc9e77c0051484e6d.jpg)

:max_bytes(150000):strip_icc()/GettyImages-157678802-27cd6fe8f49c4e79b79ebb4fa16fa040.jpg)

:max_bytes(150000):strip_icc()/investopedia-ss-reasons--people-go-bankrupt-5bfc2c8546e0fb00265c18da.jpg)

:max_bytes(150000):strip_icc()/RetirementTaxBrackets-901c5acfcbac42d189807fb3a475ff36.jpg)

:max_bytes(150000):strip_icc()/senior-man-kissing-wife-at-home-925281076-197f36771996494990761e04e99a1830.jpg)